🩸 RedBloodJournal.com

#1611 – Trump Accounts: Who Benefits?

Following the Money from Every Direction

An Opinion

Introduction

Whenever a government creates a new financial program, one question deserves to be asked before asking whether it is good or bad:

Who benefits?

Not because every program is corrupt.

Not because every politician has bad intentions.

But because every public policy redistributes benefits, risks, and opportunities among different groups.

Supporters see Trump Accounts as an investment in future generations. Critics see another financial product that ultimately enriches Wall Street more than ordinary families.

This report examines both perspectives by following the incentives rather than political party.

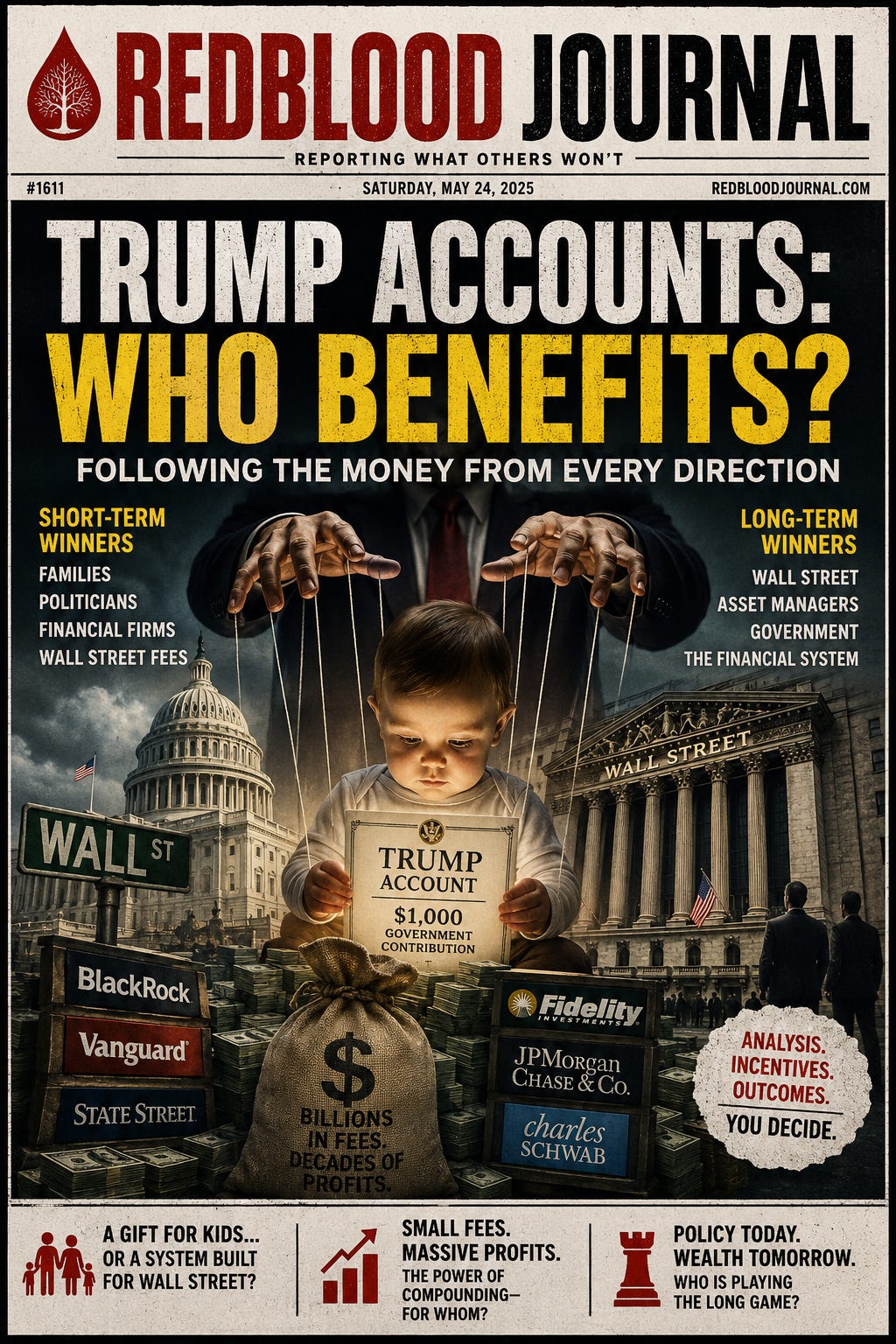

The Short-Term Winners

Families with Newborn Children

The most obvious winners are eligible families receiving the government’s initial contribution.

For many parents, it is free money that immediately begins compounding.

Politicians

Any administration introducing a program for children gains political capital.

Supporters remember benefits.

Opponents often criticize costs.

Either way, the program becomes part of the political legacy.

Investment Companies

Someone must manage billions of dollars.

That means:

Index fund providers

Asset managers

Brokerage firms

Custodian banks

earn management fees for decades.

Even extremely small annual fees become enormous when applied to millions of accounts over many years.

Financial Industry

Banks

Investment advisors

Financial planners

Software providers

Record keepers

Compliance firms

All gain new customers and new assets.

The Long-Term Winners

Children Who Leave the Money Alone

Historically, time has been one of investing’s greatest advantages.

A small amount invested over decades may become much larger if markets perform well.

Wall Street

This may be the largest long-term beneficiary.

Regardless of which political party creates the program, increasing assets under management increases fee revenue.

Billions invested today can remain invested for decades.

The longer the money stays invested...

the longer financial firms continue earning revenue.

The Federal Government

Some supporters argue these accounts encourage:

saving

investing

financial education

long-term wealth creation

which may reduce future dependence on government assistance.

Whether this outcome occurs remains uncertain.

Who Might Not Benefit?

Not everyone benefits equally.

Those born outside the eligibility window receive no initial government contribution.

Families without disposable income may be unable to make additional contributions.

Children whose investments perform poorly during extended market downturns could receive less benefit than expected.

Looking Through a Different Lens

Suppose someone intentionally wanted to increase Wall Street assets under management.

Creating millions of investment accounts would accomplish exactly that.

No conspiracy is required.

The financial incentives already exist.

Every dollar deposited becomes capital invested in financial markets.

The firms managing those investments collect fees year after year.

From this perspective, one could argue that the financial industry benefits regardless of which political party controls government.

Looking Through the Most Cynical Lens

If one chooses to examine the program from the darkest possible perspective—not as an assertion of fact, but as a thought experiment—the question becomes:

If someone cared primarily about directing trillions of dollars into financial markets, what policy would they design?

One possible answer would resemble a national investment program beginning at birth.

Under this interpretation:

families receive an immediate benefit,

politicians receive public approval,

financial firms receive decades of assets to manage,

markets receive a continuous flow of new capital.

Whether that outcome is viewed as prudent public policy or as a system that primarily advantages the financial sector depends on the reader’s perspective and the evidence they find most persuasive.

Conclusion

Every public policy creates winners.

The important question is not whether someone benefits.

The important questions are:

Who benefits first?

Who benefits most?

Who benefits for the longest time?

Sometimes the immediate beneficiary is not the largest beneficiary.

And sometimes the greatest profit belongs to those who quietly collect a small percentage from millions of people over many decades.

Whether Trump Accounts become remembered primarily as an investment in children, a stimulus for financial markets, or a combination of both will depend not only on the program’s design, but on its long-term outcomes.

The purpose of asking these questions is not to assume hidden motives, but to understand the incentives that shape public policy. By examining both the immediate and long-term beneficiaries, readers can evaluate the program on its merits while remaining aware that economic incentives often influence decisions alongside public-interest goals.

📈 The Architects of Incentive:

Who Benefits from Trump Accounts?

Jul 6, 2026

This report examines the complex incentive structures and potential outcomes surrounding the proposed Trump Accounts for national investment. While the initiative is presented as a way to provide families and children with long-term financial security, the text highlights how Wall Street firms may emerge as the primary beneficiaries through decades of management fees. The analysis explores how politicians gain capital from such programs while the financial industry secures a consistent flow of new assets regardless of market performance. Ultimately, the source encourages readers to look past immediate benefits to identify who gains the most significant advantages over time. This skeptical perspective suggests that while the accounts offer a public safety net, they also function as a massive, government-backed stimulus for financial markets.