🩸 Red Blood Journal Transmission #1241

ENRON 2.0: THE BUBBLE THAT BUYS ITSELF

Introduction

History has a strange habit of changing its clothing while repeating its lessons.

Most people remember Enron as a corporation that manipulated numbers, hid risks, and presented an illusion of prosperity until reality eventually arrived. The collapse was not merely the failure of a company; it was the exposure of a system that allowed appearance to become more important than substance.

Today, a growing number of observers are asking whether humanity is witnessing a modern version of the same phenomenon—not through a single corporation, but through an entire financial ecosystem.

The question is not whether artificial intelligence is real.

The question is whether the financial structures being built around it are.

The New Mechanism

For decades, retirement accounts, pension funds, and index funds have been marketed as safe and passive investment vehicles.

Most participants assume their money is being allocated according to neutral market rules.

But what happens when the rules themselves change?

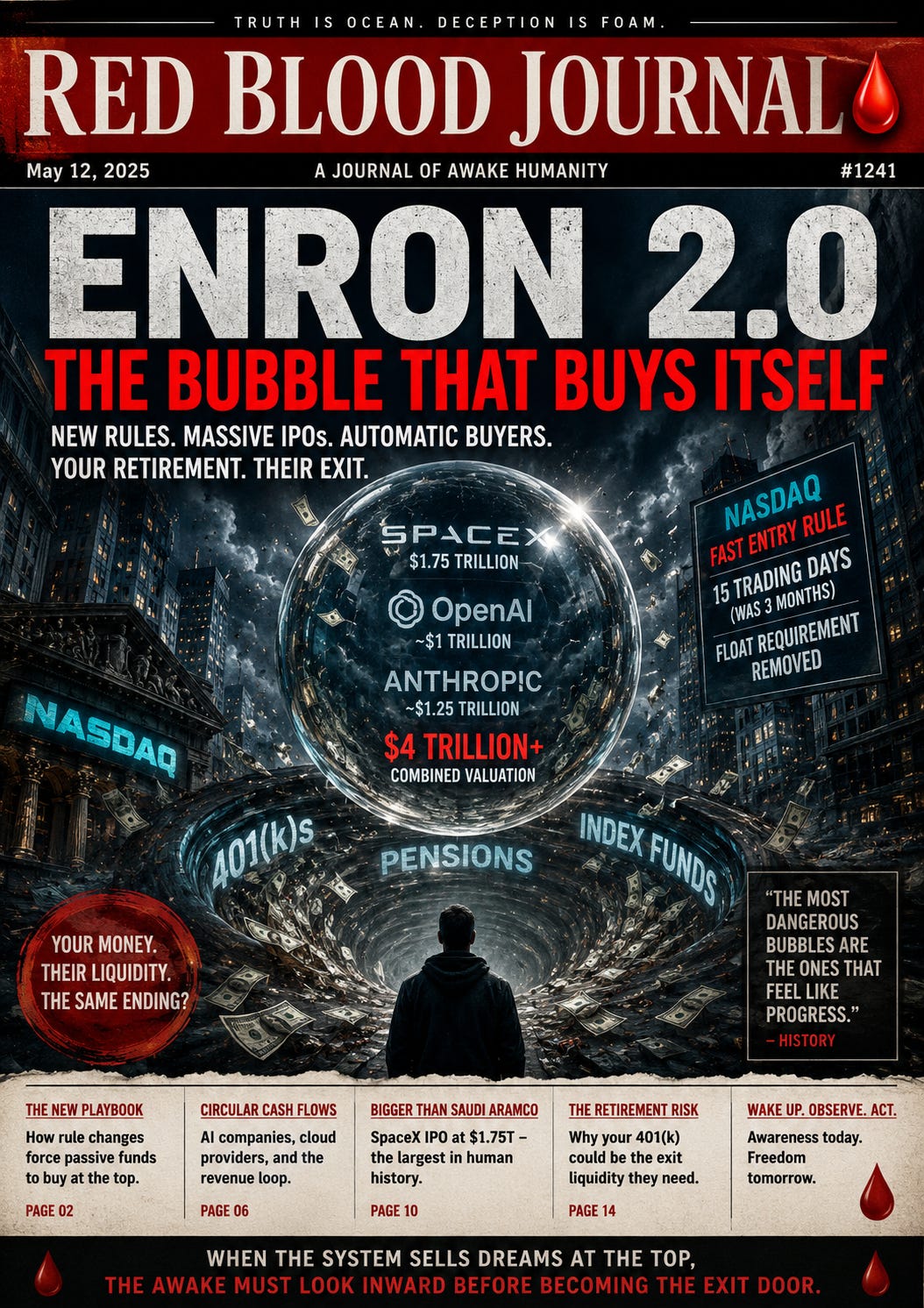

Recent discussions within financial circles have focused on accelerated index inclusion rules that could allow newly public companies to enter major indexes much faster than before.

If such companies are included rapidly, passive investment funds tracking those indexes must purchase shares automatically.

The individual saver never makes the decision.

The purchase happens because the system requires it.

The result is a mechanism where massive pools of retirement savings become automatic buyers of newly issued shares.

The Largest IPOs in History

Several technology firms are expected to seek public listings at valuations previously unimaginable.

Supporters argue these valuations reflect revolutionary technologies that will reshape civilization.

Critics argue that many valuations are being justified by expectations rather than demonstrated profitability.

The distinction is important.

A company can possess extraordinary technology while simultaneously being priced far beyond what reality can support.

History provides many examples.

Railroads changed the world.

The internet changed the world.

Fiber-optic networks changed the world.

Yet many early investors lost fortunes while the technologies themselves ultimately succeeded.

Technology and investment returns are not the same thing.

The Circle of Valuation

One of the concerns raised by critics involves what appears to be a circular flow of capital.

Large technology companies invest in AI ventures.

AI ventures purchase computing resources from those same technology companies.

Those transactions generate revenue.

The revenue supports higher valuations.

Higher valuations justify additional investment.

Additional investment creates additional spending.

The cycle continues.

As long as confidence remains intact, the circle appears healthy.

But confidence itself becomes the fuel.

When confidence becomes the primary asset, the difference between investment and speculation begins to disappear.

The Passive Investor

Traditional investing required a conscious choice.

An individual evaluated a company, accepted the risk, and invested accordingly.

The modern passive system operates differently.

Millions of people contribute automatically to retirement accounts.

Those funds automatically purchase index products.

The indexes automatically purchase qualifying companies.

The individual saver may never know what is being purchased on their behalf.

The process is efficient.

But efficiency can also create concentration.

If a small number of highly valued companies dominate the indexes, then a large portion of society’s retirement wealth becomes dependent upon the success of those same companies.

What appears diversified may, in reality, be highly concentrated.

Lessons from Enron

Enron was ultimately not about energy.

It was about trust.

Investors trusted reported numbers.

Employees trusted management.

Institutions trusted ratings.

The public trusted appearances.

Reality eventually demanded an audit.

The concern expressed by modern critics is not that AI companies are fraudulent.

The concern is that the surrounding financial assumptions may be overly dependent upon perpetual growth, perpetual demand, and perpetual confidence.

Those assumptions have historically proven fragile.

Every bubble believes it is different.

Every bubble has reasons.

Every bubble has experts.

Every bubble has believers.

Until reality arrives.

The Real Question

Artificial intelligence may transform humanity.

Space exploration may transform humanity.

Automation may transform humanity.

None of these possibilities are in dispute.

The deeper question is whether financial markets are pricing the future with wisdom or with excitement.

When excitement becomes excessive, buyers stop asking what something is worth.

They only ask whether it will continue rising.

That is often the moment when risk becomes invisible.

And invisible risk is the most dangerous kind.

Final Reflection

The greatest bubbles are rarely recognized while they are expanding.

They are usually identified afterward, when historians look back and ask why so many intelligent people ignored the warning signs.

Perhaps this moment will become another chapter in that story.

Or perhaps the future will justify every valuation and every promise.

No one knows.

But wisdom requires observation.

When the crowd is running in one direction, the thoughtful person pauses long enough to ask why.

The Ocean of Positivity does not reject innovation.

The Ocean of Positivity does not reject progress.

It simply reminds humanity that truth must always be greater than excitement, and reality must always be greater than belief.

For when illusion fades, truth remains.

And truth, like the ocean itself, cannot be hidden forever.

🩸 End of Transmission #1241

🫧 Enron 2.0:

The Artificial Intelligence Financial Bubble

Jun 7, 2026

This text draws a parallel between the Enron collapse and the current financial boom surrounding artificial intelligence, warning that enthusiasm may be overshadowing actual value.

It suggests that a circular flow of capital between tech giants and startups creates an illusion of revenue that artificially inflates market valuations.

The author highlights how passive investment systems and retirement funds automatically purchase these stocks, leading to a dangerous concentration of wealth in a few unproven entities.

While acknowledging the potential of the technology itself, the source argues that speculative excitement has made market risks invisible to the average investor.

Ultimately, the narrative serves as a cautionary reminder that financial bubbles are often built on misplaced trust and the expectation of perpetual growth.

Reality, according to the text, eventually forces an audit of such systems, potentially leaving those in automated investment vehicles vulnerable to a sudden correction.