🩸 RED BLOOD TRANSMISSION JOURNAL

T#RBJ–FINANCE–FORMULA–ARCHIVE (PART VIII)

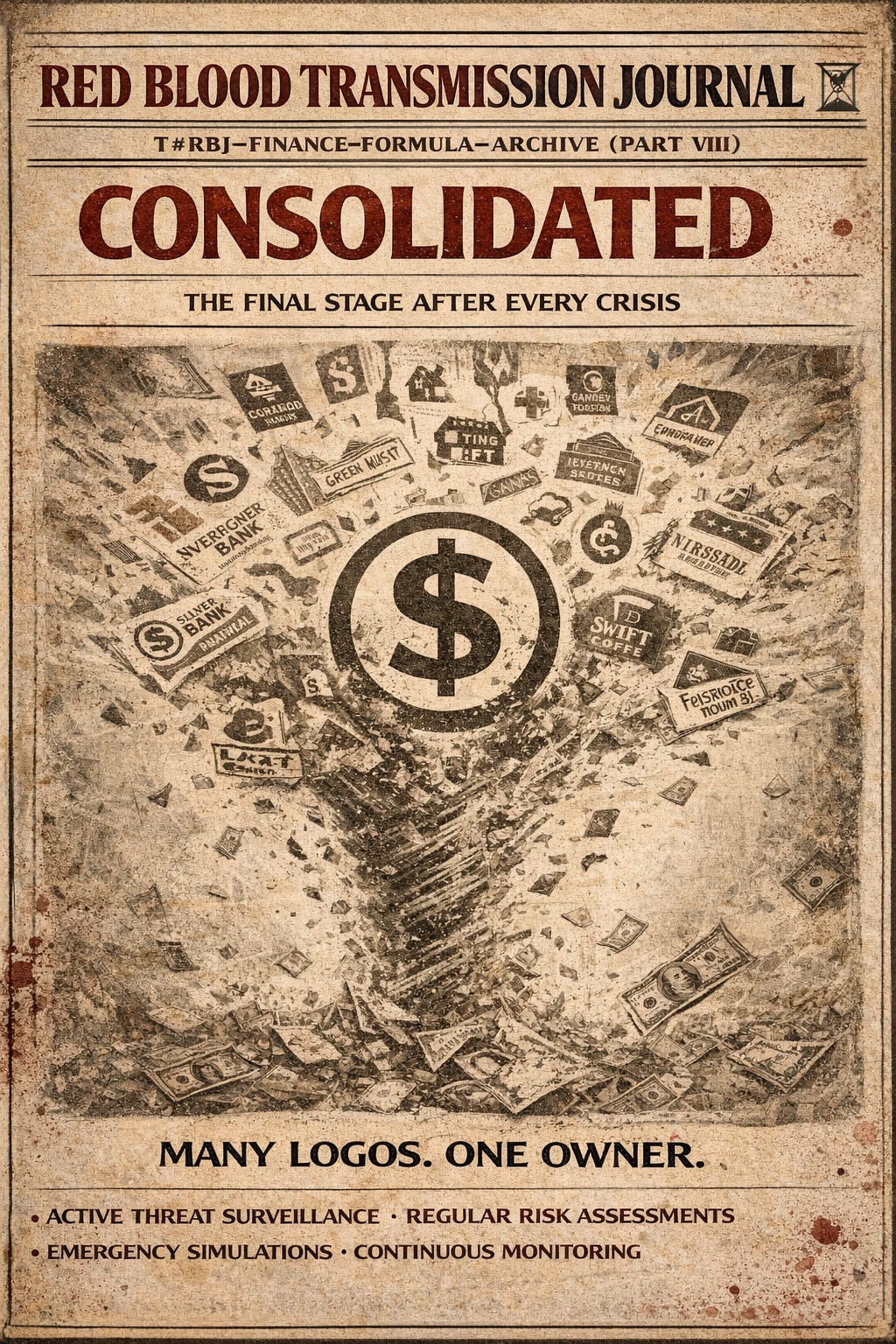

Title: Why Crises Always End With More Concentration

Classification: Power Aggregation Analysis · Market Structure

Distribution: International / Open

Method: Post-Crisis Asset Flow Mapping · Incentive Geometry · Historical Recurrence

PART VIII — COLLAPSE DOES NOT SCATTER POWER. IT GATHERS IT.

Every crisis is narrated as destruction.

In practice, crisis is sorting.

Assets don’t vanish.

They change hands.

And they do not move randomly.

I. THE IRON LAW OF CRISIS

Across financial crashes, wars, pandemics, and “once-in-a-generation” shocks, one outcome repeats:

Fewer owners. Larger owners. Deeper moats.

This is not because big actors are smarter.

It’s because they survive the valley others can’t cross.

Liquidity is gravity.

II. WHO DIES FIRST IN A CRISIS

Crises don’t hit everyone equally. They hit fragility.

The first casualties are:

small businesses with thin margins

households without buffers

local institutions dependent on cash flow

competitors reliant on credit access

These actors don’t fail because they’re inefficient.

They fail because they lack time.

III. WHO BUYS DURING PANIC

While the public experiences crisis as scarcity, capital experiences it as inventory.

During downturns:

cash-rich firms shop

private equity deploys “dry powder”

monopolies acquire competitors under “rescue” logic

regulators fast-track mergers “for stability”

The crisis compresses resistance.

What would be blocked in normal times becomes “necessary.”

IV. REGULATION AS A CONCENTRATION ACCELERATOR

Post-crisis rules rarely level the field.

They do the opposite.

New regulations:

raise compliance costs

increase reporting burdens

demand legal and technical infrastructure

Large players absorb the cost.

Small players disappear.

This is not regulatory failure.

It is regulatory selection.

V. THE MERGER JUSTIFICATION SCRIPT

Every consolidation follows the same language:

“To prevent systemic risk”

“To stabilize the market”

“To protect consumers”

“To preserve jobs”

Each phrase neutralizes opposition.

Opposing consolidation becomes framed as reckless.

Stability becomes the alibi.

VI. WHY CONCENTRATION FEELS INVISIBLE

Concentration does not arrive with tanks.

It arrives with:

paperwork

approvals

“temporary” arrangements

technical necessity

By the time the public notices, the landscape has already shifted.

Choice narrows quietly.

Dependence deepens silently.

VII. THE SCALE ADVANTAGE LOOP

Once concentration increases, it becomes self-reinforcing:

Larger entities gain policy access

Policy favors scale and “systemic importance”

Scale attracts capital

Capital absorbs competitors

Concentration increases again

The system rewards size because size reduces uncertainty for power, not for people.

VIII. WHY CRISES ARE NEVER USED TO DECONCENTRATE

Crises could be used to:

break monopolies

distribute assets

decentralize systems

They never are.

Because decentralization introduces unpredictability—

and unpredictability threatens control.

Concentration is legible.

Concentration is manageable.

Concentration is governable.

EPILOGUE — THE QUIET ENDGAME

Each crisis leaves society with:

fewer employers

fewer lenders

fewer platforms

fewer choices

The public is told the crisis “changed everything.”

It did.

It simplified ownership.

🩸 END PART VIII

Red Blood Journal — Power Aggregation Division

🧲Why Crises Always End With More Concentration

This text outlines how systemic crises function as mechanisms for wealth and power consolidation rather than mere destruction.

According to the source, economic shocks disproportionately eliminate fragile, small-scale actors while allowing well-capitalized entities to acquire assets at a discount.

These periods of instability often lead to increased regulation, which inadvertently benefits large corporations that can easily absorb high compliance costs.

The narrative suggests that stability and risk mitigation are frequently used as justifications to bypass antitrust concerns and fast-track mergers.

Ultimately, the cycle of collapse ensures that ownership becomes more concentrated, reducing public choice and making the economy easier for central authorities to manage.

This process transforms unpredictable market diversity into a simplified, more governable hierarchy of a few dominant players.