Decoding State Capitalism: A Blueprint for Small Investors in a Government-Driven Market

An Investigative Report: by Red Blood Journal

This analysis examines the U.S. government’s evolving role as a market influencer through equity stakes in strategic sectors like semiconductors, critical minerals, and infrastructure, drawing parallels to historical patterns of government intervention. It outlines three phases—early spikes, mid-term stabilization, and late-stage complacency—using examples like Intel and General Electric to highlight investment opportunities and risks. For small investors, the report identifies upsides such as stability and strategic demand, balanced against downsides like cronyism and capped growth. It recommends a “shadow index” strategy, leveraging low-fee ETFs in sectors like CHIPS Act-funded firms or DOE-backed minerals, with a buy-low, sell-high approach tied to political cycles. Looking ahead, it predicts a 2030 market split into “patriotic stocks” and “independent innovators,” offering a roadmap for non-rich Americans to build wealth by timing government involvement and pivoting to private growth.

🧩 1. The Pattern: Government as a Market Maker

When the U.S. government becomes a shareholder, it’s not just capital—it’s policy muscle.

History shows three phases when this happens:

Phase

Market Effect

Example

Early Phase (Entry)

Stock prices often spike as news spreads—investors anticipate contracts, protection, and prestige.

Intel, MP Materials after CHIPS Act funds

Middle Phase (Stabilization)

Government oversight slows innovation but ensures floor stability. Prices rarely crash hard.

Boeing, Lockheed after heavy DoD exposure

Late Phase (Complacency)

Bureaucracy creeps in, growth plateaus, and private competitors innovate faster.

General Electric post-2008 bailouts

So early investors who buy before or just as the government steps in often benefit—if they exit before political friction sets in.

💰 2. What This Means for Small Investors

Upside:

Stability Shield:

A government stake acts like a built-in safety net. The Treasury doesn’t want its equity to collapse before an election.

→ This can mean less volatility and slower drawdowns.Strategic Tailwind:

These firms are tied to national priorities: chips, lithium, rare earths, AI infrastructure. That’s the “new oil” economy.

→ Likely steady contracts, guaranteed demand.Political PR Value:

Any administration—left or right—will tout “rebuilding America.” Expect favorable headlines and incentives.

Downside:

Crony Capitalism Risk:

The more government capital enters the market, the more success depends on connections, not competition. Small investors can’t lobby Congress.Capped Growth:

These companies become quasi-utilities—safe but slow. They might not collapse, but they won’t moonshot either.Exit Trap:

Political winds shift fast. A new administration could divest or impose regulations that shock valuations overnight.

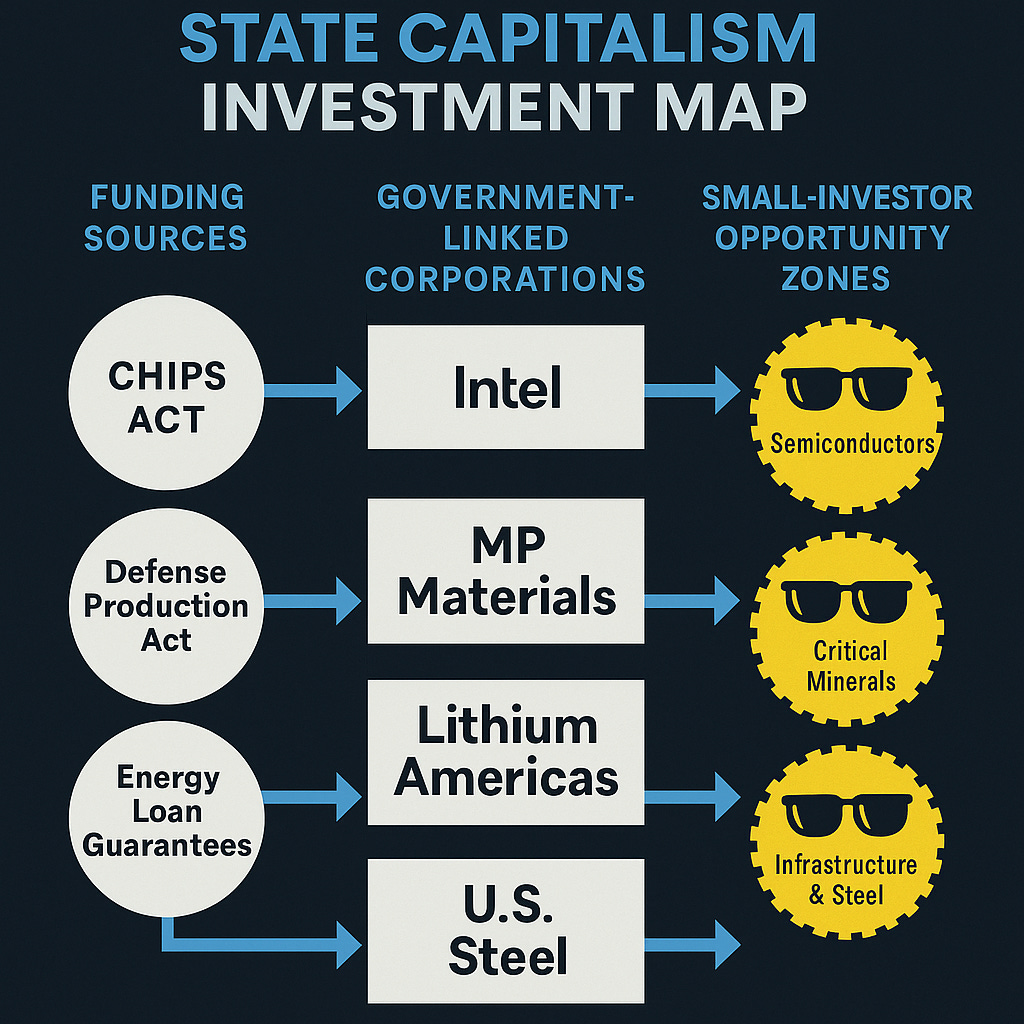

⚙️ 3. Sectors to Watch (2025–2030 Window)

Sector

Government Leverage

Investment Thesis

Semiconductors (Intel, TSMC Arizona tie-ins)

CHIPS Act funding; DoD contracts

Government won’t let domestic chip fabs fail. Slow but safe growth.

Critical Minerals (Lithium Americas, MP Materials)

Energy Dept loans, Defense contracts

Long-term hold; metals essential for EV, AI batteries. Expect supply chain nationalism.

Infrastructure & Steel (U.S. Steel, Nucor)

Golden share, domestic buildouts

Gains capped by automation and energy costs; cyclical but patriotic narrative boosts PR.

AI & Cloud Infrastructure (NVIDIA, Palantir, Oracle GovCloud)

Fed and DoD AI procurement

Wild card—these could explode in value or face antitrust heat.

🧠 4. Smart Play for Non-Rich Americans

If you’re not a hedge fund, consider the “shadow index” approach:

Track which firms receive direct federal equity, loan guarantees, or contracts via the CHIPS Act, Defense Production Act, or DOE loan programs.

Use low-fee ETFs that mirror those industrial sectors (e.g. SMH for semiconductors, LIT for lithium, URA for uranium, XLI for infrastructure).

Buy during political noise, not after the photo ops.

Rule of thumb:

Buy when Washington whispers. Sell when it brags.

🔮 5. Long-Term Prediction

If this policy continues:

By 2030, up to 15–20% of U.S. GDP could be tied to firms with partial federal ownership.

Those stocks may function as “political hedges”—less profit-driven, more policy-driven.

The market will divide into:

“Patriotic Stocks” (state-backed, steady, semi-protected)

“Independent Innovators” (riskier, faster growth, less regulation)

Small investors could thrive by riding the patriotic momentum early, then pivoting to private-sector disruptors once government saturation peaks.